The Most Efficacious Operating Model for Banks in India

The banks are crucial to the modern economy of India. These banks regulate the financial services industry. They include subsectors focusing on asset management, insurance, venture capital, and private equity.

Earlier, the core function of a bank was only limited to holding financial assets. But now, it has expanded far beyond storing gold for the wealthy financier.

According to Outlook India, The Government of India nationalised 14 private banks in 1964, including the Reserve Bank of India(RBI). In 1980, the Government of India nationalised six more private banks.

These nationalised private banks regulate the Indian economy by providing financial services. And till now, these banking sectors are dominating and leading the financial industry in India.

The financial sector is booming and has come so far. But with the growing customer needs and the need to maintain the vast economy, regular upgradation of operating models in banks should be incorporated to anticipate trends and challenges ahead.

According to Newsroom Accenture, banks can increase annual revenues by nearly 4% by embracing innovations and banking operating models.

This operating business model will deliver value to internal and external customers of the financial sector and improve its core structure.

Why is the Operating Model necessary for the regulation of banks?

The banking sector is constantly evolving and will continue to grow in the upcoming years. New technologies and advancements in the banking industry are continuing to implement ground-breaking financial products and services.

The strategic innovations in the banking sector through crowdsourcing, piloting, collaborations and partnering are persistently progressing to develop revolutionary banking solutions.

With the ever-changing banking sector, new regulations and revised strategies have been developed through the bank business model. An Indian bank should always use operating models as a tool to help them formulate and execute its strategy.

A study by McKinsey has shown that 80% of the growth comes from a company’s way of management, including the structured operating framework, and the rest of 20% comes from the secondary industries.

We at GrowthJockey unlock any organisation’s full growth potential through strategic execution.

Our operation models include the following elements:

-

Maps

-

Charts

-

Blueprints

-

Matrix and People Models

-

Scorecards

-

Decision grids

What is the Most Productive Operating Model for Banks in India?

The digital mindset is the key to organisational success. It is about creating a customer-centric culture. It is based on constantly looking to improve the quality of user experience and ensuring that customer needs are satisfied.

Organisations can stay ahead of the curve by following a digital mindset and strategies and capitalising on the latest trends and technologies. By embracing digitisation, banking sectors have introduced new technologies to enhance customer satisfaction and services.

Banks have already begun increasing technology companies to keep pace and face competitors. But they must still rethink their talent needs and prioritise digital-forward talents like technologists, data engineers, and non-traditional hires.

Further, banks must develop a new digitally advanced operational environment to power the entire sector. Additionally, they should embrace technologies based on unique digital experiences to meet these objectives.

This includes creating a future operating model in banks that facilitates data-driven decision-making, drives operations with new technology, and aligns effort with reward in the front office.

When it comes to knowing the most productive operating model for banks in India, Digital Operating Model is the topmost among all the other operating models in finance industry.

Here's the explanation of why this model stands at the top and is the most constructive for the banks and the financial sector.

Why is the Digital Operating Model Potent for the Banking Sector?

The COVID-19 pandemic has changed consumer habits and the financial sector forever. Many organisations have pivoted operations and entered the digital field. In contrast, others that did not have been left behind.

But why do organisations need to go digital— especially the banking sector? The question is valid. Before you put banks into digitisation, it is necessary to understand what going digital really means and how it will translate to banks.

Imagine a world where data is seamlessly shared across your business, enhancing consumer experiences and increasing operational efficiencies.

Integration and automation in banks save costs, save time, cut down on errors, and make better use of human resources.

This approach contributes to personalised interactions and self-service alternatives, generates new revenue opportunities on various digital platforms, and satisfies customers' rising expectations.

Models like data-driven credit decision models shorten the underwriting and lending cycles and boost the system's capacity.

A patchwork strategy does not work in this fast-paced world. The cornerstone for banks must be based on the Digital Operating Model, where data is at the core and flows throughout the value chain.

So, when a consumer supplies their information, it can guide internal decision-making, provide goods and services to customers, and speed up growth.

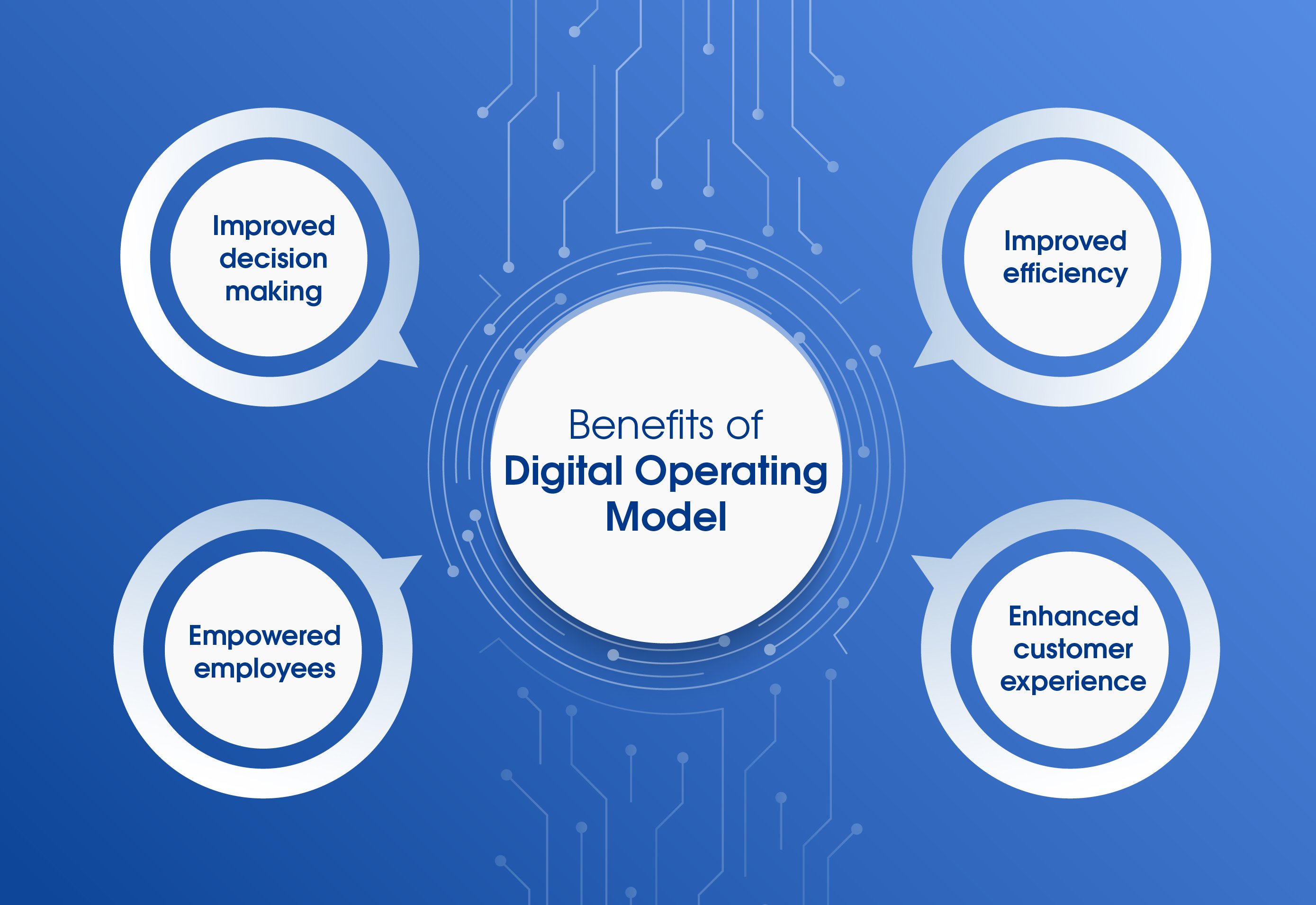

Benefits of the Digital Operating Model

Going with the Digital Operating Model can accelerate organisations' operations and processes. Through this model, tasks that take hours to complete can be reduced to mere minutes or seconds by letting intelligent technology take over.

Four benefits pave the way for digital transformation to do more within the banks. They are more sustainable, more data-driven, and more compliant. Read on to discover why banks should ditch traditional methods and introduce a new Digital Operating Model.

Improves decision making

Digital Operating Model involves many critical decisions based on the latest facts, including redefining current manufacturing and production processes, validating new techniques, and assessing technology.

It is digitally easier to track the progress data and can help to reveal patterns and trends through the digital models in bank.

Improves efficiency

Digital Operating Model can be essential in creating lean and well-organised processes. It can help reduce or eliminate duplications and setbacks in the workflow. Furthermore, It allows banks to speed up by automating specific tasks.

Empowers employees

Having the right technological tools that work together can streamline workflow and improve productivity. Automating many manual tasks and integrating data throughout the organisation empowers team members to work more efficiently.

Improves customer experience

Digital Operating Model provides a hassle-free experience at every point in their journey with your business. While a digitised business is vital in attracting new customers, it is equally important in retaining existing ones by providing seamless and quick communication.

Bottom-Line

An operating model connects an organisation’s strategy with its operational capabilities. Strategy is ‘why and what a company does’, while operations are ‘how the company does things.’ These two concepts align together in the Digital Operating Model.

It provides a guide for management to follow when turning strategic goals into operational abilities.As it is known that Digital Operating Model is the most productive model to proceed with the banking sector, banks can now follow the digitisation of frameworks to enhance their growth.

Understanding how various digital advancements collect, categorise, and store data is essential to make effective decisions and to keeps biases from crawling into the predictions.

As necessary, financial sectors and banks need to learn how to present data persuasively to turn visions into action. A robust Digital Operating Model prioritise upskilling the essential resources while aligning them to value-add activities.

The banking sector picked up pace in the post-COVID phase. As stated by Money Control, it is expected to grow 15-16 per cent in 2023.

Planning digital transformation through a Digital Operating Model by GrowthJockey to identify new tools will help the business to achieve better results. Their models create a culture of operating for finance management that is receptive to change.

Exceeding new data is being generated, created, and evaluated every day by utilising digital technology. Banks must constantly switch from one set of bank business models to the next in a digital world— so that they can embark on massive change initiatives and not have to wait for the next disruption.

At GrowthJockey, we are fully committed to developing customised operating models that effectively address the critical challenges faced by our clients across various industries. Irrespective of your company's size, whether it's a small-scale enterprise or a large corporation, you can now benefit from our tailored solutions. Take the decisive step towards unlocking the next level of growth for your brand by reaching out to us today!